Artea Bank 2025 Q4 financial review

A year of decline

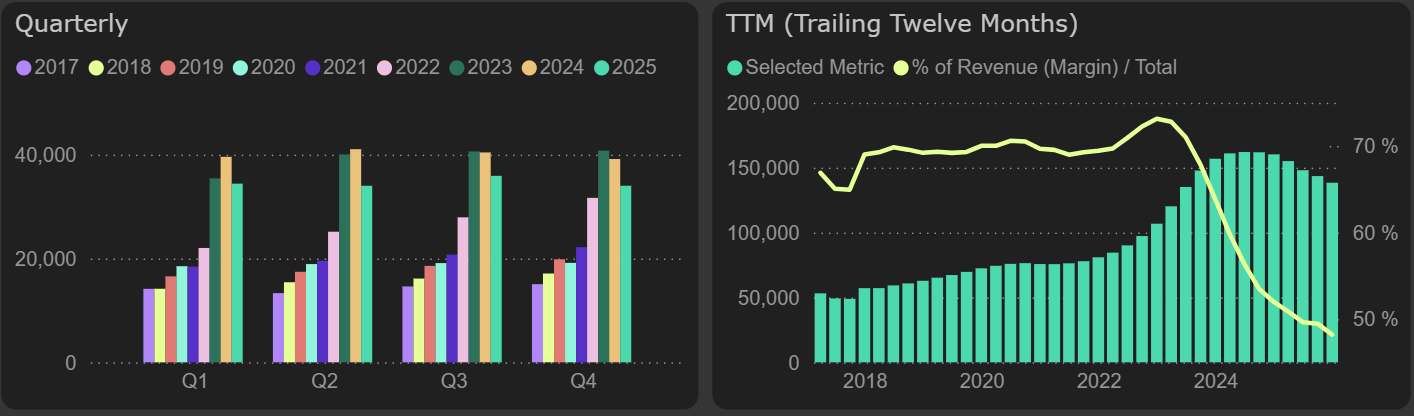

Artea Bank did not show a recovery by the end of 2025: although net interest income in the third quarter was 6% higher than in the second quarter, it returned to the second quarter level in the fourth quarter. Meanwhile, Coop Pank and LHV Group demonstrated stronger net interest income at the end of the year than in the third quarter.

Annual net interest results fell by 14% YoY at Artea Bank and LHV Group, and by 6% YoY at Coop Pank. However, in the comparable period, i.e., in 2024, Artea Bank and LHV Group were still growing, while Coop Pank's results were already declining.

Net interest income

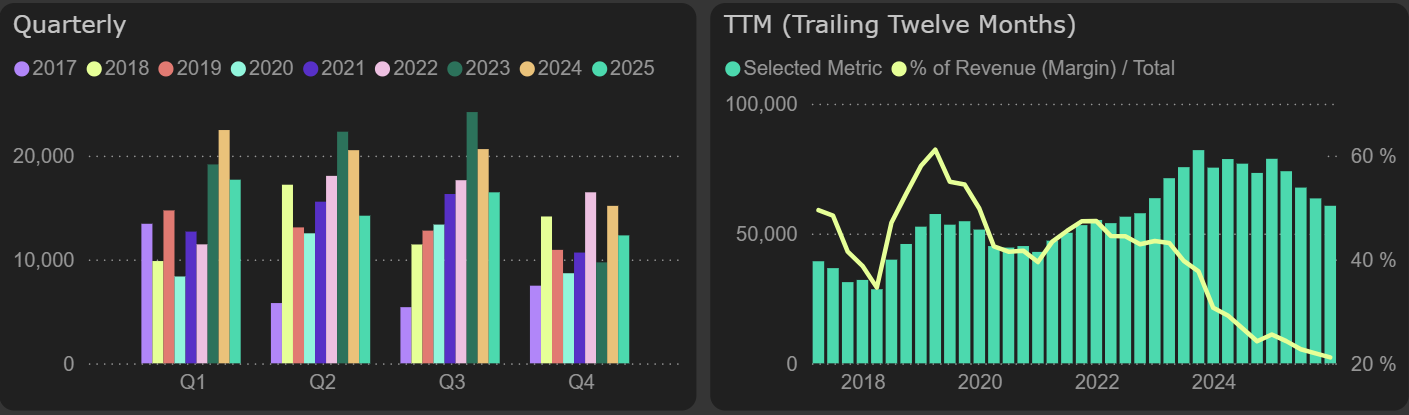

In the fourth quarter, Artea Bank's net profit was 19% lower than a year earlier, and the annual profit fell by 23% to €60.7M. LHV Group's net profit dropped by 22%, while Coop Pank's fell by 11% (with growth recorded in the fourth quarter).

Net profit

All three banks faced the same challenges in 2025 – declining net interest income and rising operating expenses.

Artea Bank's other operating expenses were €10.7M higher (+28% YoY), mainly due to IT and communication costs, while staff expenses increased by €5.6M (+11% YoY).

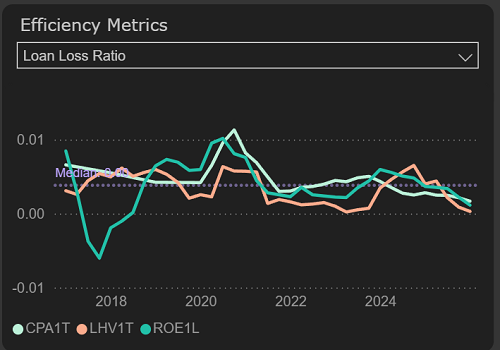

Lower impairment expenses supported 2025 results – particularly for Artea and LHV. However, while all three maintain strong loan loss ratios, any deterioration in credit quality would add further pressure on profitability.

Loan loss ratio

By market valution metrics, Artea Bank does not stand out: its P/E is higher than that of Estonian banks, and its ROE is the lowest. Artea's P/BV is similar to Coop Pank and lower than LHV Group, but LHV Group justifies its premium with significantly stronger ROE.

Furthermore, Estonian banks showed twice as strong loan portfolio growth in 2025 – around 20%, compared to only 8% growth at Artea Bank.

Comparison between banks