TKM Grupp 2026 Q1 financial review

Stronger start of the year

TKM Grupp started 2026 stronger than 2025. In the first quarter of this year, revenue was 6% higher than a year ago. The main driver of growth was the car trade segment, where revenue increased by 49% YoY, supported in part by recent acquisitions. However, the core segment – supermarkets – saw revenue decline by 4% compared to last year.

The EBITDA margin in Q1 remained unchanged compared to last year, resulting in EBITDA growing at a similar pace to revenue — up 5% YoY. As both sales and margins improved in the car trade segment, its EBITDA more than doubled compared to the first quarter of last year. Meanwhile, the supermarkets segment put additional pressure on overall performance, with EBITDA declining by 27%, and turning loss-making after depreciation.

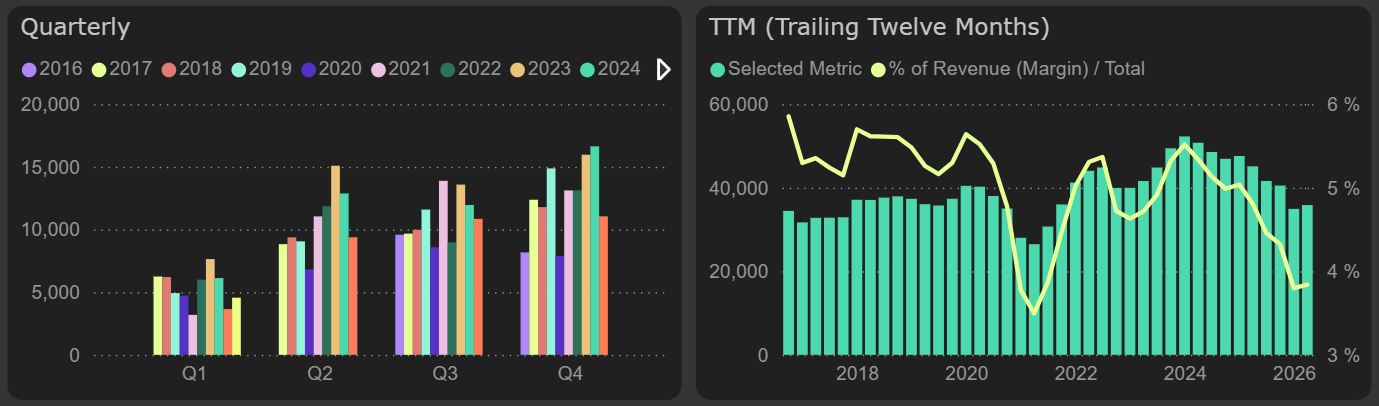

Results by segments, 2026 Q1

Depreciation recognized in Q1 2026 was slightly lower than last year, which, in the context of growing sales, had a positive impact on the operating profit margin. As a result, operating profit increased by 25% YoY, reaching €4.6M.

However, this result is not exceptional in the company’s historical context – stronger Q1 results were achieved in 2022–2024, when operating profit ranged between €6M–€7.6M.

Operating profit

As is typical for the first quarter, dividend-related taxes resulted in a net loss, although it was smaller than last year.

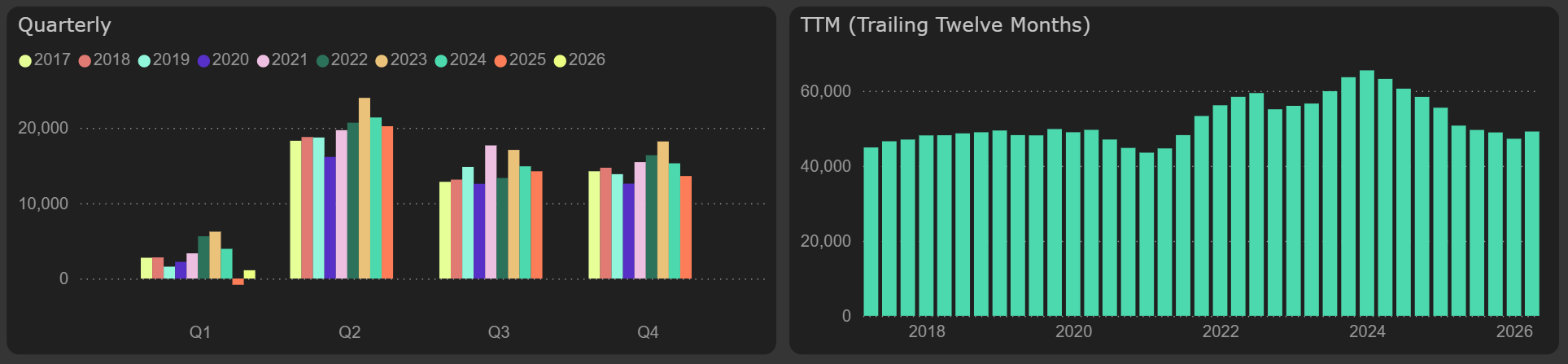

Acquisitions required €21M in net cash outflows in Q1 2026, while funds from operations amounted to just €1M, resulting in negative free cash flow for the quarter. Although FFO in the first quarter is typically significantly lower than in other quarters, this year’s figure was relatively weak in a historical context, despite being higher than last year.

Funds from operations

Valuation metrics remains high and not particularly attractive: P/E 19.6x, EV/EBITDA 9.6x. Meanwhile, ROE is at its lowest level in the past 15 years, at 8%.